Filters - Mathematical Background

The process of filtering, which comprises smoothing as a special case,

can be described mathematically in several equivalent ways:

Linear Algebra

Smoothing can be performed by moving a window over the signal and averaging

data points within the window. In a more general setting it is a weighted

average, where the weighing factors are called filter coefficients. We

can split the weighted average approach into two calculation steps:

-

an element-wise multiplication of the data points with the filter coefficients

-

summing all the weighted points in the window

This is identical to a dot product of two vectors, where one vector consists

of the data points in the window and the other vector of the filter coefficients.

We can include the selection of the window in the dot product by setting

the values for the filter coefficients outside of the window to zero, so

our data vector will be the whole signal. The moving of the window requires

us to use a different vector for the filter coefficients for each move

or shift. This results in a series of vector dot products, which

can be assembled into one matrix multiplication.

Convolution

The mathematical operation of convolution

(often represented by a star) is decribed by the following equation:

.

Here x is the noisy signal, h stands for the filter coefficients,

y

is the smoothed signal, and

j is the index to the data points, while

i

is the index for the filter coefficients. In the case that we have 2n+1

filter coefficients, the index i runs from -n to +n. So our data

window stretches only n points to the right and left of the data point

under consideration. This approach is computationally more efficient than

the matrix multiplication approach, where the windowing has to be done

by a large number of multiplications by zero. .

Here x is the noisy signal, h stands for the filter coefficients,

y

is the smoothed signal, and

j is the index to the data points, while

i

is the index for the filter coefficients. In the case that we have 2n+1

filter coefficients, the index i runs from -n to +n. So our data

window stretches only n points to the right and left of the data point

under consideration. This approach is computationally more efficient than

the matrix multiplication approach, where the windowing has to be done

by a large number of multiplications by zero.

When we pay close attention, we see that the convolution equation is

for time-reversed filter coefficients, since we multiply h(-n) by x(j-(-n))=x(j+n).

For most of the smoothing filters this has no meaning, since the coefficents

are symmetric around the middle value.

Convolution in the Fourier Domain

It can be shown that the convolution in the Fourier domain can be represented

by the following equation:

The capitalized variables stand for the Fourier-transformed variables y,

x and h. The frequency is depicted by

ω. In

the Fourier domain convolution reduces to an element-wise multiplication

of the signal and the filter coefficients. H is also called impulse reponse,

since it is obtained by setting the signal x equal to an impulse, i.e.

it is zero everywhere except for one data point that is '1', and convolving

it with h. The Fourier transform of the result of the convolution between

this signal x and h is equal to H and is called impulse reponse.

The capitalized variables stand for the Fourier-transformed variables y,

x and h. The frequency is depicted by

ω. In

the Fourier domain convolution reduces to an element-wise multiplication

of the signal and the filter coefficients. H is also called impulse reponse,

since it is obtained by setting the signal x equal to an impulse, i.e.

it is zero everywhere except for one data point that is '1', and convolving

it with h. The Fourier transform of the result of the convolution between

this signal x and h is equal to H and is called impulse reponse.

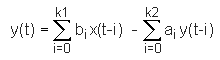

State Space Notation

The most general form of describing filters is the so-called state-space

notation:

.

It is a generalized version of the convolution equation we gave above.

Here the filter coefficients are given by ai and bi

and the index i runs from 0 to ki instead of -n to +n. The second

sum on the right includes contributions of already filtered data points.

Depending on whether the filter coefficients ai and bi

are zero, the filters have different properties and names. .

It is a generalized version of the convolution equation we gave above.

Here the filter coefficients are given by ai and bi

and the index i runs from 0 to ki instead of -n to +n. The second

sum on the right includes contributions of already filtered data points.

Depending on whether the filter coefficients ai and bi

are zero, the filters have different properties and names.

-

When all the bi coefficients are zero, the filter is called

an

Infinite Impulse Response (IIR) or recursive filter. Auto-regressive

(AR) random processes can be produced by applying this filter to random

inputs.

-

When all the ai coefficients are zero, the filter is called

Finite

Impulse Response (FIR) or non-recursive filter. Moving average (MA)

random processes can be produced by applying this filter to random inputs.

|

Bivariate Data

Bivariate Data